Recently, I dug into recent financial results of several downstream crude oil refiners. I am a fan of the energy subsector, but I was surprised at how well these companies can and will perform in the current energy price environment.

So surprised that I was happy to add a new refiner stock to my dividend growth-focused investment service recently.

Here’s why – and three refiners to consider for your own portfolio…

Successful fuel refining companies are some of the best-managed businesses in the U.S. They operate in an industry where the prices of both the raw materials (crude oil) and finished products (gasoline and other fuels) are set by outside market forces. Refiners have to live with whatever the commodity markets give them.

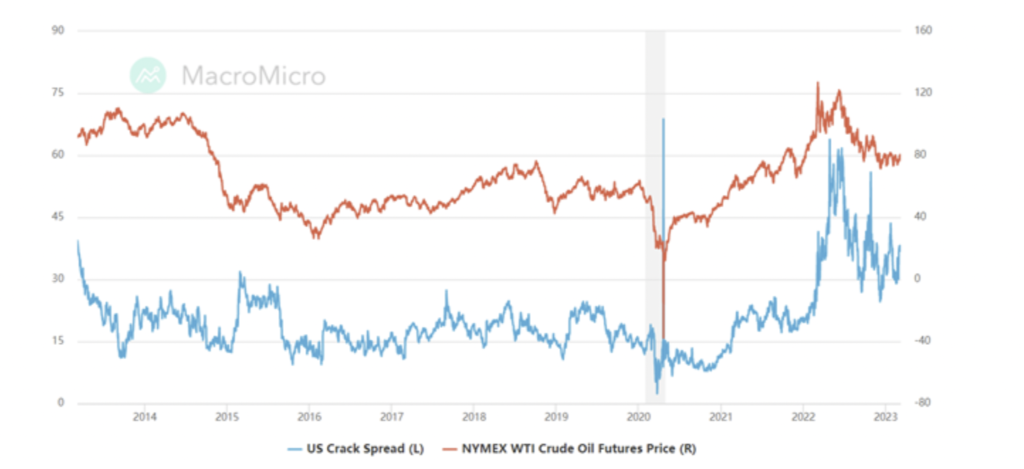

Refining profitability relates to the crack spread. The spread is the calculation of the price difference between refined products and the cost of a crude oil barrel. The benchmark 3-2-1 crack spread is the difference between three barrels of oil, two barrels of gasoline, and one barrel of distillates (diesel, jet fuel, heating oil). Put another way, the crack spread is the gross profit margin per barrel of oil when refined into fuels.

A modern, efficient refinery has an operating cost of $5.00 to $8.00 per barrel. Factor in other corporate expenses, and you get a breakeven at around a $10.00 crack spread. On this chart, the blue line is the U.S. crack spread with the corresponding value on the left side of the chart:

Over the decade, the crack spread ranged from a low of $7.50 in early 2020 to more than $58.00 last Spring. Historically, you can see the spread tended to be in a range of $15.00 to the low-$20s. The Russia-Ukraine war caused the prices of crude oil and fuels to spike higher, pushing the crack spread to record levels.

Next, let’s look at the same chart for the last six months:

If you watch the financial news, you may have observed that crude oil trading has been relatively stable, in a $70 to $80 range. You may also have noted that gasoline at the pump has been stable for several months. In my area, every station shows regular unleaded at $3.29 a gallon.

The recent price stability, from the end of November to the present, kept the crack spread locked in at $30 to $35 per barrel. At these levels, the refining companies are hugely profitable. Let’s look at the fourth quarter results from the three large independent refining companies:

- Marathon Petroleum Corporation (MPC) reported earnings of $6.65 per share, compared to $1.30 a year earlier

- Phillips 66 (PSX) reported earnings of $4.00, up from $2.94 in the last quarter of 2021

- Valero Energy Corp (VLO) reported $8.45 per share, up from $2.47 per share

If you annualize the Q4 earnings, these companies trade at a P/E ratio ranging from 4 for VLO to 6 for PSX. On a fundamental evaluation, these stocks are very cheap.

I expect the price of oil and the crack spread to stay current. We are already most of the way through the 2023 first quarter, and you can see that profits this quarter will be excellent.

I have one of the three listed refining companies in the portfolio for my Monthly Dividend Multiplier service, which employs a dividend growth strategy. This month I am adding a smaller regional refining company. Now is a great time to get overweight in the downstream energy space.