Last week, the financial news media went crazy when the Treasury yield curve inverted. If you listened to the news, you likely thought that the economy was sitting on the verge of a recession.

But let’s talk about what the current yield curve really has to tell us.

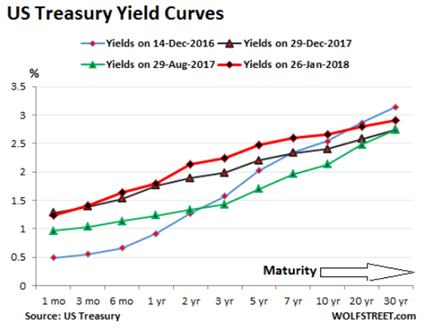

The Treasury yield curve plots current Treasury bills, notes, and bond interest rates against their time to maturity. In “normal” times, the yield curve has a positive slope, meaning the interest rates (or yields) are lower in the shorter-term and higher in the longer-term. This chart of the curve from dates in 2016, 2017, and 2018 shows a positive slope (source: Wolfstreet.com):

An inverted yield curve occurs when longer-term rates are lower than shorter-term rates. At the short end of the curve (a year or less), rates are set by the Federal Reserve Fed Funds Rate. For maturities of two years out to 30 years, rates are set by trading in the bond markets.

Analysts and media pundits often look at the “2-10 yield curve,” which is the difference in yield between the two-year and 10-year notes. Just those two data points.

Now let’s look at some of the realities of what an inverted yield curve means.

An inversion of the yield curve preceded every economic recession in recent history (going back to the Great Depression). The recessions followed the initial inversion by six to 18 months.

However, the contra-positive is not the case. The yield curve has gone inverted at other times, and a recession did not occur. A yield curve inversion is not a 100% predictor of recessions.

Last week, the inversion that created all the excitement amounted to just two basis points. A basis point is one hundredth of a percent. So, the two-year yield was just two-hundredths of a percent above the 10-year yield. In my mind, two basis points is noise and not an inversion. It’s a flat yield curve, and flat yield curves do not predict anything.

My final thought on this subject is theoretical: in this world, with thousands of analysts, writers, bloggers, and business news network commentators, an inverted yield curve will not sneak up on investors or the economy. With perfect, universal knowledge of the state of the yield curve, I am suspicious of whether it still has any predictive power.

In the past, the fact that an inverted yield curve “predicted” a recession was determined after the economy went into negative growth. It was a backward-looking indicator, and I am skeptical if an inverted curve can be used as a forward predicting indicator.Bottom line, the recent “inversion” of the yield curve should not be a factor in your investment decisions. Of greater concern should be positioning your portfolio to benefit from higher interest rates and continued inflation. That is where I am leading my Dividend Hunter subscribers. 20,000 thousand of them are already “immune” to the effects of inflation – to join them, click here.