Since the pandemic, Rithm Capital (RITM) has dramatically expanded its business operations; it now functions as a global asset manager. But, the market continues to price RITM as if it were still a narrowly focused finance REIT.

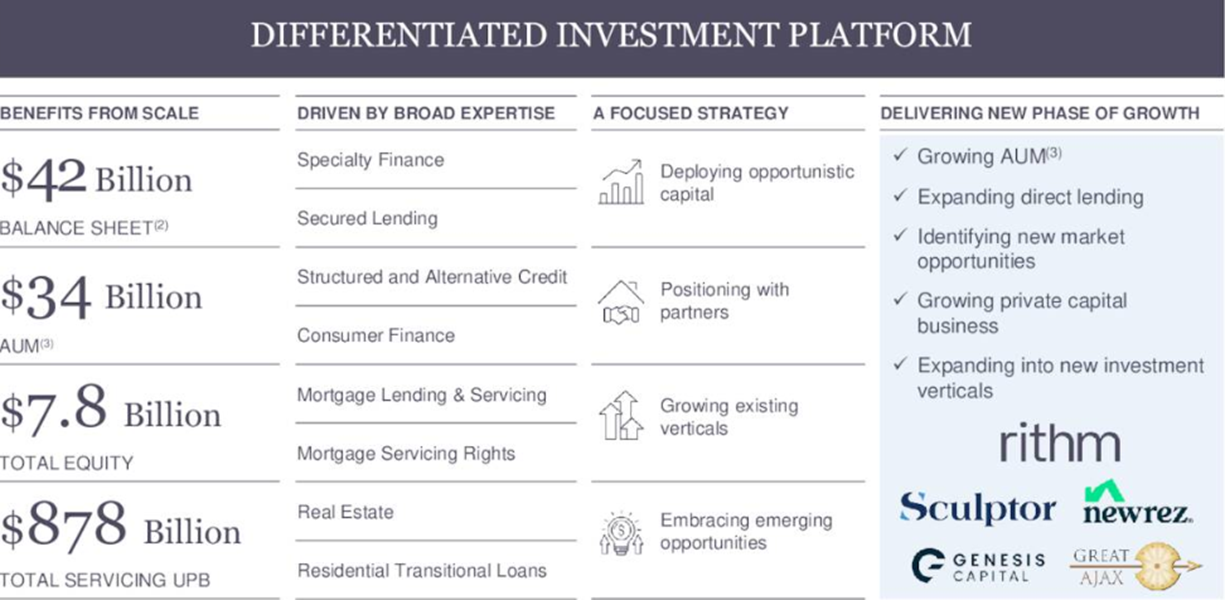

Over the last few years, Rithm has expanded its business to offer a wide range of finance and lending solutions. This chart from the third quarter earnings presentation shows the range of services the company now offers.

The two middle columns tell the tale of Rithm’s business diversity. The growth in products and strategies has produced growing profits. Earnings available for distribution per share have grown by 60% since 2021. Over the last four quarters, Rithm generated distributable earnings of $2.00 per share.

RITM shares have traded in a $9.00 to $12.00 range for the last three-plus years. As noted earlier, earnings grew by 60% over that period, and the book value increased from $11.50 to $12.50 per share. The $2.00 per share in distributable earnings and the current $11.00 share price mean that RITM trades for just five-and-a-half-times earnings and at a 12% discount to book value.

Rithm has paid the current $1.00-per-share annual dividend since the third quarter of 2021, and the current yield is an attractive 9%. I know investors are disappointed that the company has not increased its dividend to match the growth in distributable income, and that might be one cause for the stagnated share price.

Still, even without growing the dividend, Rithm Capital should trade at a premium to book value, not a discount. I believe RITM could be a $15.00 stock within the next year.

Why is Amazon suddenly paying 39.70%?

Something big is happening with Amazon stock...

While most investors collect ZERO dividends from Amazon...

A small group just discovered a “backdoor” way to collect yields up to 39.70%!

And here’s the really strange part:

It’s completely legal...

It\’s surprisingly simple...

Yet most financial advisors have no clue it exists